How to Fund an Earnest Money Deposit (EMD) Without Giving Up Equity

You've found the deal. The numbers work. The seller is motivated. But the purchase contract requires a $150,000 earnest money deposit — and tying up that capital for 45 days of due diligence means freezing your liquidity at exactly the wrong moment. The instinct is to call an equity partner. That instinct is costing you a fortune.

1. The Liquidity Trap in Deal-Making

The Problem

In commercial real estate, M&A, and search fund acquisitions, the earnest money deposit is the price of admission. It signals to the seller that you're serious — and it gives you the contractual right to perform due diligence before committing to close.

But here's the trap: EMDs are illiquid capital. Whether it's a soft deposit that's refundable during the inspection period or a hard deposit that goes non-refundable at a specific milestone, that money is locked up — sometimes for 30, 60, or even 90 days — while you underwrite the deal.

For a sponsor running multiple deals simultaneously, or a search fund entrepreneur who has spent months finding the right acquisition target, tying up $100,000 to $500,000 in a single deposit can freeze your entire deal pipeline.

The Instinct

Most sponsors reach for the phone and call an equity partner or co-GP. It feels like the obvious solution: someone else puts up the deposit capital, you get the deal under contract, and you figure out the economics later.

The problem is that "figure out the economics later" almost always means giving away a significant slice of your deal's upside — permanently — in exchange for what is fundamentally a short-term liquidity solution.

The Hook: There Is a Better Way

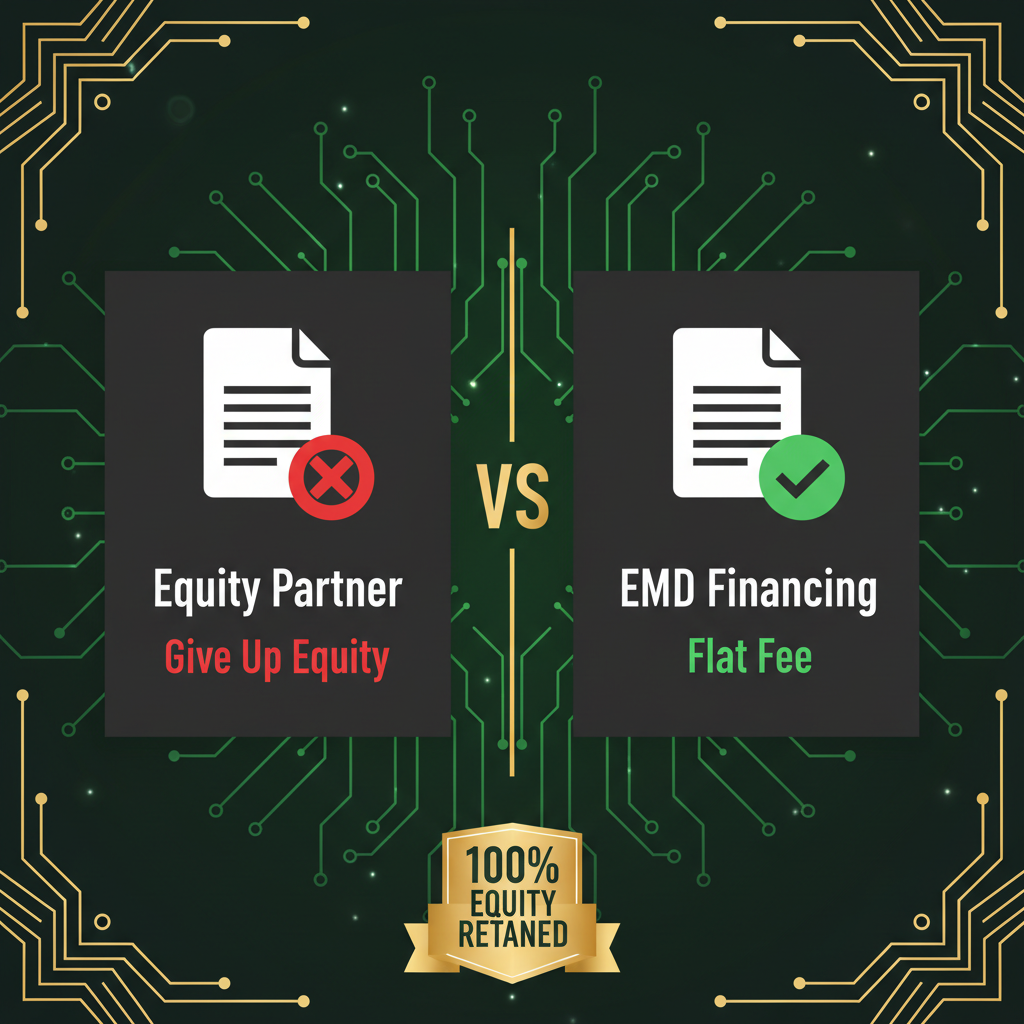

Giving away 10% to 30% of a deal's back-end upside just to cover a temporary deposit is one of the most expensive mistakes in deal-making. The alternative — non-dilutive EMD financing — lets you secure the deal, preserve your equity, and pay a predictable, flat fee at closing.

2. Why Using Equity Partners for EMD Is an Expensive Mistake

The True Cost: Run the Math

Let's make this concrete. Imagine a $5 million commercial acquisition where the equity partner agrees to fund a $100,000 EMD in exchange for 15% of the GP equity.

On a deal that generates $800,000 in GP-level profit over a 3-year hold, that 15% stake is worth $120,000 — paid to someone who contributed capital for 45 days of due diligence and then stepped back.

The reality: You are paying an implied annualized rate of over 120% for what is essentially a 45-day bridge loan. No rational borrower would accept those terms from a bank — yet sponsors accept them from equity partners every day because the cost is invisible until the exit.

Loss of Control

The financial cost is only half the problem. When you bring in an equity partner to fund your EMD, you are handing them a seat at the decision-making table before the deal is even fully underwritten.

Economic Retrading

Once an equity partner has skin in the game, they gain leverage to renegotiate deal terms during due diligence — often demanding better economics in exchange for not pulling their deposit capital.

Approval Bottlenecks

Every major decision — from extending the inspection period to adjusting the purchase price — now requires partner sign-off, slowing your ability to move at deal speed.

Permanent Dilution for Temporary Capital

The equity stake granted for EMD funding is typically permanent. You are solving a 45-day liquidity problem with a 3-year (or longer) ownership concession.

3. Three Ways to Fund EMD Without Equity Partners

There are three legitimate, non-dilutive paths to funding your earnest money deposit. Here's how each works — and where each falls short.

Transactional / EMD Financing — The Best Alternative

Specialized niche lenders — like EarnestBridge — exist specifically to provide short-term capital for earnest money deposits. This is the cleanest, most efficient solution for deal-makers who want to preserve their equity and move fast.

How it works: You submit your deal (LOI or purchase agreement), the lender reviews the transaction, and wires the deposit directly to escrow — typically within 24 to 72 hours. At closing, you repay the principal plus a flat fee or small percentage. No equity. No profit sharing. No ongoing obligations.

✅ Zero equity dilution — you keep 100% of your deal upside

✅ Predictable, flat-fee pricing — no surprises at the closing table

✅ Non-recourse structures available — the deal backs the loan, not your personal assets

✅ Fast funding — 24 to 72 hours in most cases

✅ Works across CRE, M&A, search funds, and energy leases

Best for: CRE sponsors, M&A deal-makers, and search fund entrepreneurs who want to protect their equity and close deals quickly.

Negotiating the LOI / Purchase Contract

Before you fund anything, consider whether the deposit structure itself can be negotiated. Sophisticated buyers sometimes structure deposits to minimize upfront capital exposure:

The caveat: In competitive markets — particularly for stabilized CRE assets or high-quality business acquisitions — sellers routinely reject staged deposits and LOCs. If you're competing against all-cash buyers or institutional sponsors, creative deposit structures can cost you the deal entirely.

Personal Capital or Unsecured Lines of Credit

If you have existing corporate liquidity or access to an unsecured business line of credit, deploying that capital for an EMD is a legitimate option — and it keeps your equity fully intact.

✅ No equity dilution

✅ No lender approval process

✅ Immediate access if capital is already available

⚠️ Concentrated exposure — if the deal falls through and the deposit goes hard, you absorb the full loss

⚠️ Opportunity cost — capital tied up in one deposit can't fund other deals in your pipeline

⚠️ Unsecured lines often have variable rates and can be recalled by the lender

Best for: Sponsors with deep corporate liquidity who are running a single deal at a time and have high conviction in the transaction.

4. What to Look For in an EMD Financing Partner

Not all EMD lenders are created equal. If you're evaluating a dedicated EMD financing partner, here's the checklist that separates serious capital providers from opportunistic ones.

Speed: Funds Wired in 24–72 Hours

CriticalDeals move fast. When a seller executes your LOI and expects a deposit within 48 hours, you need a financing partner who can match that timeline. Ask specifically: "What is your average time from deal submission to wire?" If the answer is longer than 72 hours, keep looking.

Non-Recourse: No Personal Guarantees

Non-NegotiableThe best EMD financing programs are structured around the deal — not your personal balance sheet. A non-recourse structure means that if the deal falls through and the deposit is forfeited, the lender absorbs the loss, not you. Avoid any EMD lender who requires a personal guarantee, co-signing rights, or access to your personal financial statements.

Flexibility Across Verticals

ImportantMany EMD lenders are narrowly focused on residential real estate wholesaling. If you're a CRE sponsor, M&A deal-maker, or search fund entrepreneur, you need a partner who understands your deal type. Ask whether they fund commercial acquisitions, business purchase agreements, energy leases, and M&A transactions — not just residential flips.

Transparent, Flat-Fee Pricing

ImportantAvoid lenders who price based on a percentage of your deal profit or who bury fees in complex term sheets. The best EMD financing partners provide a Proforma Invoice upfront — showing your exact cost before you commit to anything. Flat-fee or utilization-based pricing (e.g., a daily rate on capital deployed) is far more predictable than profit-share arrangements.

Minimal Documentation Requirements

Good to HaveA good EMD financing partner qualifies the deal, not the borrower. You should need to provide a signed LOI or purchase agreement, the EMD amount, and a clear path to closing — not tax returns, personal financial statements, or years of business history.

5. Conclusion: EMD Is a Capital Problem, Not an Equity Problem

The earnest money deposit is a temporary capital requirement. It exists for 30, 45, or 90 days — and then it either converts to a down payment or gets returned. It is not a long-term investment. It is not a partnership. It is not a reason to give away 15% of your deal's back-end upside.

Protect your equity for the long-haul investors — the LPs, the co-GPs, the institutional partners who are contributing capital, expertise, and relationships over the full hold period. Don't dilute that equity pool to solve a 45-day liquidity problem.

The most sophisticated deal-makers in commercial real estate, M&A, and search fund acquisitions have already figured this out. They use dedicated EMD financing platforms to secure deposits quickly, preserve their equity entirely, and keep 100% of their deal upside — paying a predictable, flat fee at closing instead of surrendering a permanent ownership stake.

Keep 100% of Your Deal Upside

EarnestBridge provides fast, flat-fee, non-recourse EMD financing for commercial real estate sponsors, M&A deal-makers, and search fund entrepreneurs.

- ✅ Funds wired in 24–72 hours

- ✅ No personal guarantee required

- ✅ Zero equity dilution — flat fee at closing

- ✅ CRE, M&A, search funds, and energy leases

Frequently Asked Questions

What is non-dilutive EMD financing?+

How fast can I get an earnest money deposit loan?+

Does EMD financing require a personal guarantee?+

Can EMD financing be used for M&A and search fund deals?+

Why is using an equity partner for EMD a mistake?+

Continue Reading

Share this article